The Challenges of a Credible Transition Pathway and How to Deliver It

![]()

Both investors and corporate management teams struggle with transition plans. Many CEOs have released climate change targets, some of which aim to be 1.5°C aligned by 2030 and/or net zero by 2050. More recently, nature transition plans are being developed with a goal of becoming nature positive. Investors and lenders need to understand how these pathways will be achieved and calculate the appropriate risks and opportunities against a fluid policy and regulatory backdrop.

Transition plans – Transition plans demonstrate how corporates intend to move from their existing operating model – a business as usual (BAU) scenario – to one which is better aligned with key global environmental goals – the change scenario. To minimise disruption from this transformation, some companies have developed time-bound climate transition plans which aim to align their operations with limiting global warming to 1.5°C above pre-industrial levels by 2030, and/or net zero emissions by 2050. Some companies are also implementing energy transition plans alongside this, which go beyond decarbonisation, such as considering diversification into other low-carbon industries. Nature transition plans are also beginning to emerge, with the goal of making their businesses nature positive.i The Global Biodiversity Framework outlines 23 action-oriented global targets by 2030.

These transition plans can be assessed by financial markets and used to evaluate investment opportunities and mitigate transition risks. Risks include the likelihood of companies being left behind as uncompetitive in a new business environment, while opportunities could include a first-mover advantage with new markets and pricing power.

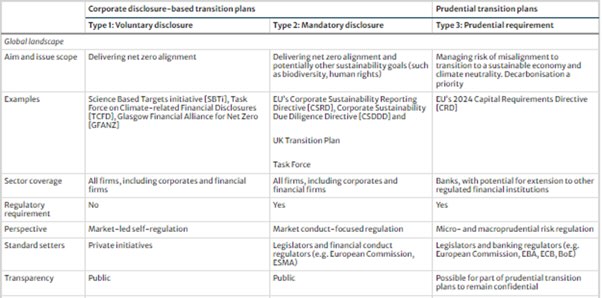

A useful analysis of the main types of transition plans are identified in a paper ‘Prudential net zero transition plans: the potential of a new regulatory instrument’.ii See Table 1.

Initially, voluntary net zero alignment plans emerged in mid-2010s to the early 2020s. These included the Science Based Targets initiative [SBTi], Task Force on Climate-related Financial Disclosures [TCFD], and Glasgow Financial Alliance for Net Zero [GFANZ]. Some of these gave rise to later offshoots such as the Taskforce on Nature-related Financial Disclosure [TNFD], which was launched in September 2023.

Next, in the mid 2020s, were the mandatory disclosures which were also net zero aligned but started to include other sustainability goals such as biodiversity and human rights. These included such initiatives as the EU’s Corporate Sustainability Reporting Directive [CSRD], Corporate Sustainability Due Diligence Directive [CSDDD].

Both the first and second stages were corporate disclosure-based transition plans, but the authors suggest that a third stage will include a prudential based approach, which will aim to manage the risk of misalignment to transition to a sustainable economy and climate neutrality. They expect decarbonisation to be the priority.

Table 1: Emerging typology of transition plans. For the full table please see the source paper. (Source: Dikau, S., Robins, N., Smoleńska, A. et al)iii

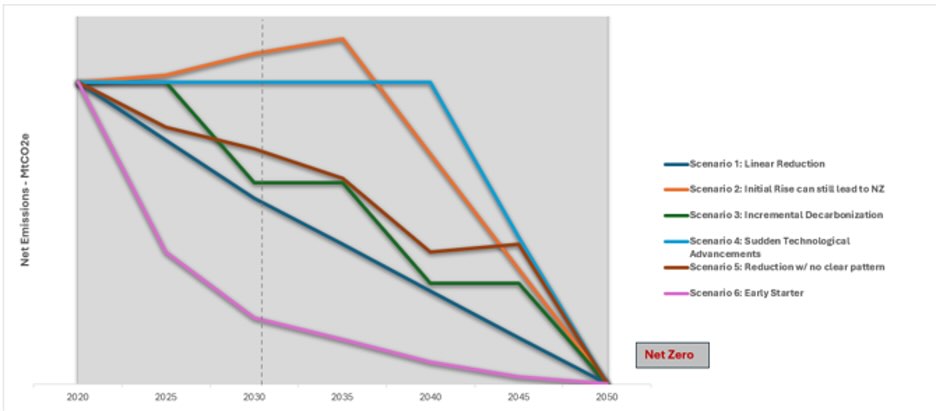

Analysing the pathway – A major challenge for financial institutions is determining which trajectory the transition pathway will take and whether the net zero target will be achieved by 2050. Where companies have set science based targets and transition plans, their decarbonization pathway will be aligned with a carbon budget: the total cumulative greenhouse gas (GHG) emissions permitted over a period of time to keep global temperature rise below a certain temperature threshold, in most cases below 1.5°C.

Figure 1 shows a range of theoretical pathways that five notional companies, all starting at the same net emission point, all reach a net zero end-point. In terms of predictability, the preference will be for an orderly (negative) linear pathway (scenario 1), which provides a high level of predictability and keeps a company within its carbon budget.

But it is entirely reasonable that the net zero emission pathway will be non-linear and disorderly, as many variables could be involved. For example, a company could initially increase its net emissions before achieving a dramatic decrease in the later years (scenario 2). Perhaps the most common scenario is likely to be a stepped one, in which technology reduces carbon emissions, but in stages as it becomes operational or the technology improves (scenario 3). Some of these scenarios would see a company exceed their carbon budget, meaning they are not aligned with a 1.5°C pathway.

Figure 1: Theoretical Net GHG emissions pathways to net zero by 2050 (Source: Planet Tracker)

Market timing “The only problem with market timing is getting the timing right” – Peter Lynch

To win the financial market’s confidence, management teams could invest heavily in GHG emissions reduction technologies to demonstrate their intention to reduce GHG emissions. But this strategy comes with risks, particularly where technologies are in the early stages of development.

Ideally, management teams would like to be in line with Government policy to minimize systematic risk. This could mean either taking action to reduce GHG emissions, if Government policy is supportive of this – i.e. going green in a greening world – or taking no GHG abatement measures, as Government policy does not promote emission reduction – i.e. a collective failure on climate mitigation – see Figure 2.

Figure 2: The individual versus the world – Source: ‘What planet are we on?’ Mark Cliffeiv

What is most risky for executive teams and investors is being out of line with Government policy – i.e. going green before required by Government policy or ignoring green policies, leaving the company exposed to regulation.

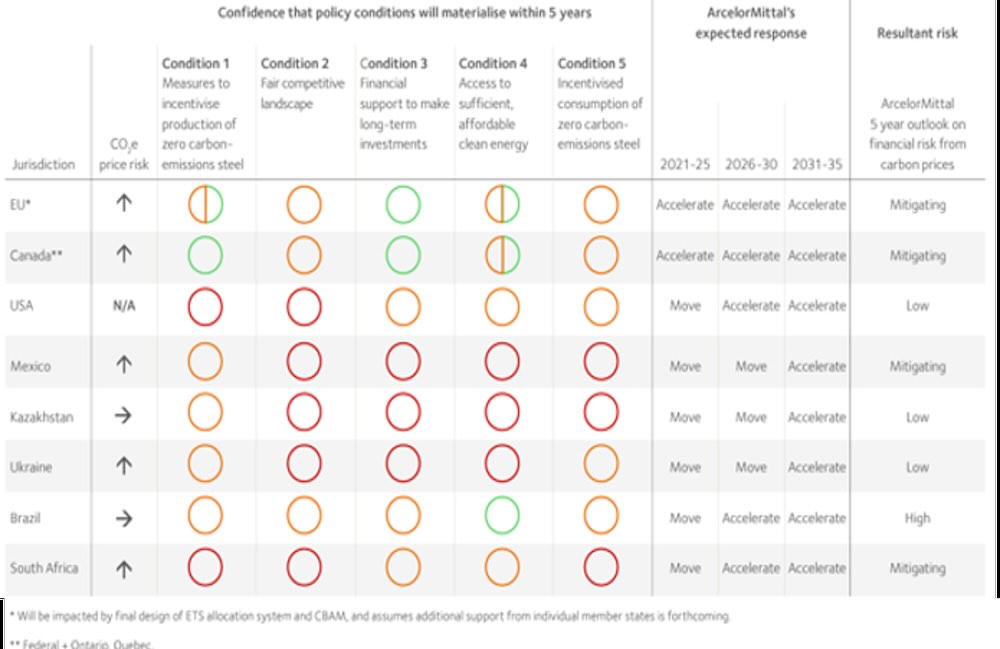

Some companies disclose detailed policy risk analysis showing where they are positioned in terms of upcoming Government policies. For example, ArcelorMittalv has conducted an assessment to understand emerging policies that would enable zero carbon steel production – see Figure 3.

Figure 3: The role of policy in ArcelorMittal’s Climate Action Plan (2021). Source: https://corporate-media.arcelormittal.com/media/ob3lpdom/car_2.pdf

The symmetry of stranding – too late or too early?Often, the risk of stranded assets – i.e. those assets which incur early or unanticipated write-downs or devaluations – is viewed as asymmetrical. For example, if a production process fails to remain compliant with environmental requirements, there is a possibility that it will cease to operate and will be financially valued at zero. However, stranding can also occur if a corporate runs well ahead of environmental regulations. For example, a company begins to implement carbon mitigation technology such as carbon capture and storage (CCS) – but it proves technically difficult to scale, too costly or is uncompetitive because the expected carbon pricing regulation is not introduced and therefore needs to be retired prematurely as superior technologies emerge.

The routes to decarbonisation vary by sector. Some key strategies include improved energy efficiency, improved material efficiency and circular economy strategies, industrial electrification, low-carbon industrial processes, low carbon fuels & feedstocks.

More contentious is whether carbon offsets and credits should be used when calculating net emissions of CO2. And should they only be used as a final resort?

Financial exposure – So how hard should financial institutions push companies to invest in new transition technologies? At a simple level, they are likely to push management teams if they see significant dangers of a company being left behind by competitors or if regulatory exposure is rising. But, if this is not the case, there must be a temptation to encourage executives to return free cash flow to shareholders (in dividends and share buybacks) or pay down debt to reduce interest costs, rather than make long term investments in decarbonisation or nature positive strategies. It’s a classic example of whether to take a short pay-off or bet on a long term return.

What appears strange to Planet Tracker is that most of the transition strategy and analysis appears under non-financial reporting. However, we view these decisions as very much embedded in finance – e.g. how to allocate cash flow or what risks and opportunities should be priced in.

Ideally, the financial markets desire economic sectors to transition at the lowest possible risk with the highest return. And if there is an imbalance, particularly a high risk to low return probability, will financial institutions discourage the corporate from adapting?

For those financial institutions running climate transition funds, a minimal engagement strategy could prove very risky. Will fundholders call out asset managers of transition or Paris-aligned funds if most of their investments remain well above the 1.5°C target in 2030? Or will financial regulators take on this role? At some stage between now and 2030, a major improvement in corporate transition deliverables is needed to avoid this confrontational scenario.

Delivering credible transition plans – Planet Tracker believes that there are some climate transition plans which should give financial markets some comfort. In our report ‘Tomorrow’s Chemistry,vi we compare the climate transition plans of the seven chemical companies in the Climate Action 100+. Leaders and laggards can be clearly identified.

Best practice on credible transition plans involves the following:

- Disclose Carbon Footprint: Ensure transparent climate-related reporting by measuring and disclosing all relevant greenhouse gas emissions across Scopes 1, 2, and 3. This is fundamental to understanding the company’s full emissions footprint, setting a baseline for targets and tracking progress.

- Define a Decarbonisation Strategy: Develop a comprehensive, science-based strategy to achieve decarbonisation targets. This should include specific actions and scalable technologies that the company will implement to reduce emissions.

- Establish a Timeline: Define a clear and realistic timeline for achieving decarbonisation milestones. Regularly update and communicate progress to stakeholders to ensure accountability and transparency.

- Detail Capital Expenditure: Provide a detailed breakdown of the capital required to implement the transition plan. This includes the total amount of investment and the timing of expenditures, ensuring alignment with decarbonisation goals.

- Plan Net Emission Reductions: Specify planned net emission reductions at a granular level, such as individual plants or operations, including quantified emissions reductions by action and technology type. This helps in assessing whether the stated targets are achievable and provides clarity on the expected impact.

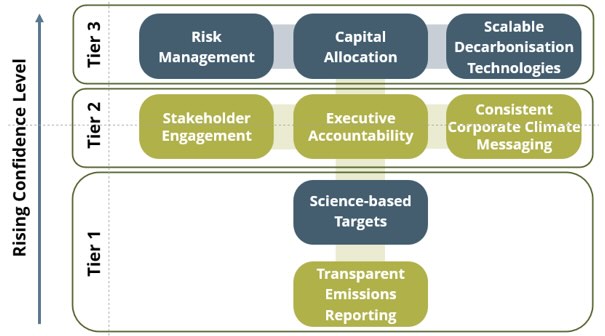

In Figure 4 we outline how financial operators can gain increasing confidence in climate transition plans as they move from tier 1 to tier 3.

Figure 4: How financial institutions can have increased confidence in climate transition plans (Source: Planet Tracker)

We accept that nature transition pathways to deliver a nature positive outcome are being rapidly developed and are more likely to result in more regional or local outcomes . Planet Tracker encourages readers to examine the Business for Nature high-level actions using the assess, commit, transform, and disclose (ACTD) approach.vii Actions for individual sectors towards a nature positive future are also available.viii

Navigating the obstacle course – Delivering on transition plans can be challenging. In truth, some CEOs probably signed climate pledges believing they were distant promises, so there was plenty of time to set a strategy. Recall the Glasgow UNFCCC Conference of Parties (COP 26) in 2021. But many Paris-aligned targets are now five years away from their delivery date, and if major project investment is required, operationally this could be demanding.

Nature transition is also required with many biodiversity targets for sovereign states deliverable by 2030.ix Among the 23 targets, within the Global Biodiversity Framework, Target 15 explicitly mentions companies and financial institutions. It requires “large and transnational companies and financial institutions to regularly monitor, assess, and transparently disclose their risks, dependencies and impacts on biodiversity, including with requirements for all large as well as transnational companies and financial institutions along their operations, supply and value chains, and portfolios”.x Initiatives such as the TNFD are beginning to provide corporates and financial institutions with guidance for integrating nature into decision making.

Encouragingly, there are examples of corporate best practice which could be applied or modified. Financial institutions should be heavily engaging with corporates on such issues as it not only impacts the risk/return profile of their investments, but a failure to deliver on this transition could make them vulnerable to claims from fundholders or regulators, especially those which manage transition and carbon-linked investments. Prudential authorities are also likely to join this fray.

Closing Thoughts – The path to credible transition plans is complex but essential for aligning with global climate and biodiversity goals. Both investors and corporate leaders need to navigate this landscape with transparency, strategic foresight, and a commitment to science-based targets. Transition plans should include clear timelines, detailed capital expenditure, and granular emission reduction strategies to provide a comprehensive roadmap for achieving net zero emissions and nature-positive outcomes.

Financial markets play a crucial role in evaluating these plans, balancing the push for innovative technologies with the caution against premature investments. As sustainability regulations evolve, the alignment with government policies and prudent management of potential stranded assets are key to mitigating risks.

In summary, delivering effective transition plans requires a concerted effort from all stakeholders. By integrating best practices and fostering collaboration, companies and financial institutions can lead the way towards a sustainable future, ensuring economic sectors transition smoothly and responsibly. The urgency for action is clear, and there are tools and guidance available for achieving these goals. What remains is the commitment to develop and execute these plans with diligence and integrity.

i Nature Positive Initiative – A Global Goal for Nature: Nature Positive by 2030

ii Dikau, S., Robins, N., Smoleńska, A. et al. Prudential net zero transition plans: the potential of a new regulatory instrument. J Bank Regul (2024)

iii Dikau, S., Robins, N., Smoleńska, A. et al. Prudential net zero transition plans: the potential of a new regulatory instrument. J Bank Regul (2024)

iv Mark Cliffe – The Actuary – What planet are we on? (4 May 2023)

v ArcelorMittal’s Climate Action Plan (2021).

vi Planet Tracker – Tomorrow’s Chemistry (April 2024)

vii Business For Nature – High-level business actions on nature.(Accessed June 2024)

viii Business For Nature – Sector actions towards a nature positive future (Accessed June 2024)

ix Convention on Biological Diversity – The Biodiversity Plan: 2030 Target (with guidance notes)